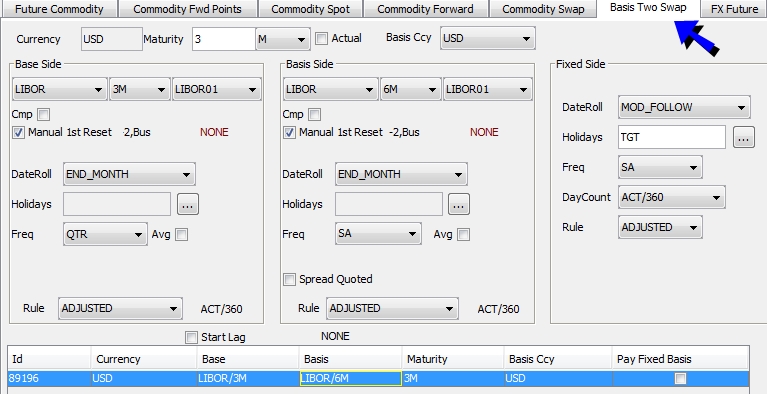

Basis Two Swap - Curve Underlying

The Basis Two Swap underlying allows specifying a spread between two swap trades.

Before you begin

| • | Create rate indices using Configuration > Interest Rates > Rate Index Definitions from the Calypso Navigator. |

Creating a Basis Two Swap Underlying

The basis two swap underlying has two floating indices and a fixed rate, and can be cross-currency.

| » | Select a currency at the bottom of the window. |

You can click Load to load any existing underlying.

| » | Click New to create a new underlying. |

Complete the basis swap fields as described in the Basis Swap Underlying.

See Basis Swap Underlying for details.

See Basis Swap Underlying for details.

Complete the fixed side fields described below.

| » | Click Save to save the underlying. It is given a unique ID by the system, and is displayed in the table. |

Fields Details

| Fields | Description |

|---|---|

|

Pay Fixed Basis |

Check to pay the fixed side, or clear to receive the fixed side. |

|

DateRoll |

Select the date roll convention. From the Calypso Navigator, navigate to Help > Date Roll Conventions for details. |

|

Holidays |

Select holiday calendars. |

|

Freq |

Select the payment frequency. |

|

DayCount |

Select the daycount convention displayed from the rate index definition. |

|

Rule |

Select the accrual period adjustment rule on non-business days. |