Capturing Asian / Lookback Equity Structured Options

An Asian Strike and Rate option, or Asian In and Out, is one where the Strike and Final reference level of the option is the average of one or more fixing dates.

An Asian Rate option, or Asian Out, is one where the Final reference level of the option is the average of one or more fixing dates.

The Asian/Lookback payout allows the user to create a option trade using Asian and Lookback characteristics.

Choose Trade > Equity > Equity Structured Option to open the Equity Structured Option worksheet, from Calypso Navigator or from the Trade Blotter.

| » | Select the Asian / Lookback payout. |

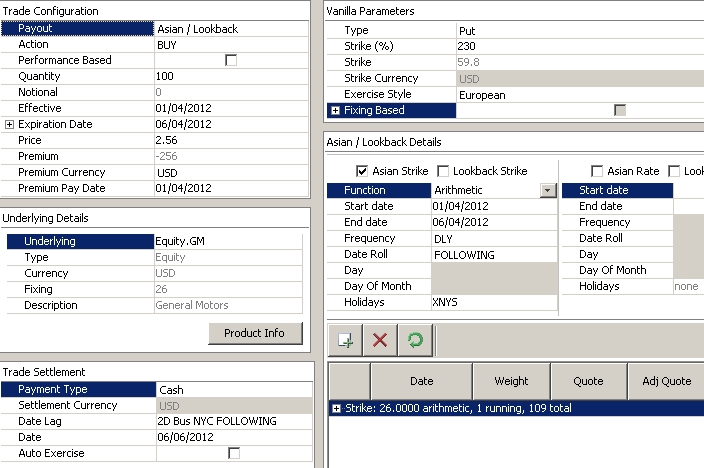

Equity Structured Option Trade Window - Sample Asian Strike trade

See Capturing Equity Structured Options for general details.

See Capturing Equity Structured Options for general details.

Asian / Lookback Details

Asian or average rate options derive the final spot as the arithmetic or geometric average of a series of pre-specified dates.

| » | Select the type of option: Asian Strike, Lookback Strike, Asian Rate, Lookback Rate. |

| » | Then enter the fields described below as needed. |

| » | The observation schedule is generated. You can modify the weight of each observation date. |

You can click  to add an observation date as needed.

to add an observation date as needed.

You can click  to regenerate the observation schedule.

to regenerate the observation schedule.

| Fields | Description | ||||||

|---|---|---|---|---|---|---|---|

|

Function |

Select the averaging function for Asian options.

|

||||||

|

Start Date |

Select the start date of the observation period. |

||||||

|

End Date |

Select the end date of the observation period. |

||||||

|

Frequency |

Select the observation frequency. |

||||||

|

Date Roll |

Select the date roll convention when the observation date is not a business day. |

||||||

|

Day |

Enter the day of the week for weekly frequencies. |

||||||

|

Day of Month |

Enter the day of the month for monthly frequencies. |

||||||

|

Holidays |

Select the holiday calendar to determine business days. |