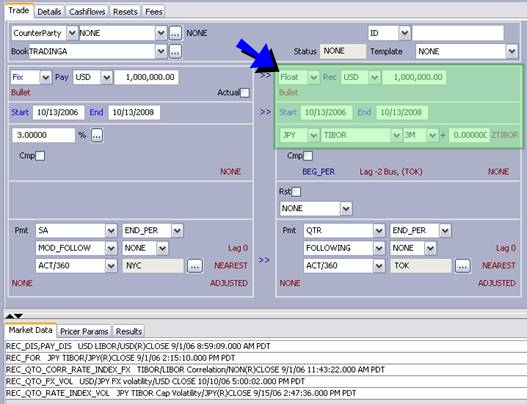

Capturing Quanto Swap Trades

A Quanto Swap is an interest rate swap where the currency of the notional on the floating leg differs from the currency of the reference index.

Choose Trade > Interest Rates > Swap to open the Swap worksheet, from the Calypso Navigator or from the Trade Blotter.

The floating leg notional is in USD, and the reference index is in JPY. Payments occur in USD, but using JPY rates.

| » | Enter swap details in the Trade panel |

| » | Then enter more trade details as described in Capturing Swap Trades. |

Cashflows

Select the Cashflows panel for displaying the cashflows.

Select Cashflows > Configure Columns to select columns specific to Quanto Swaps:

- QTO_ADJUSTMENT

- QTO_CORR_RATE_INDEX_FX

- QTO_FX_VOL

- QTO_RATE_INDEX_VOL